The one about gen-AI

Friends,

I hope that all is well with you and yours, and that this e-mail finds you on a boat with shoddy connection, in the tropics, three months after I sent it.

Now accepting keynotes for 24Q4-25Q1

Every year, I create three main presentation decks. For 2024, they are:

What to Do When You Don’t Know What to Do: How to turn uncertainty into a competitive advantage. (Based on my new book by the same name.)

Regression Toward the Meme: Why modern leadership falls into old traps - and how to avoid them.

The Efficiency Illusion: How to uncover the hidden costs of digital commerce and create profitable growth.

If you want to book me for your event, corporate speaking slot, or workshop, merely send me an email. To make sure I am available, please do so at your earliest convenience; my availability is limited and the schedule is filling up fast. More information may be found here.

A couple of updates before we go-go

First, foremost, and most importantly, a happy birthday to my brother who turned 40 yesterday. I have long said that the best man I have ever known is my father; if I ever become half the man he is, it would be twice as much as I could ever hope for. Well, my brother is undoubtedly the man closest to being him - and that is the highest compliment I am capable of giving anyone.

I am immensely proud, to the extent that it is in my right to be, of the person he has become, and continue to look up to him even though I am the elder child.

I say it far too seldom, but I love you, my brother. And always will.

On a less jubilant but more personal note, the last week has been (outside of birthday celebrations) r-o-u-g-h. I will not bore you with the details, but it is has been a veritable comedy of relentless misfortunes relating to everything from our two year-old daughter’s health to potential financial hits in the range of tens of thousands of dollars.

Just on and on and on it goes.

I am getting very tired of it all. Tired of the relentless setbacks. Tired of the lack of breaks. Tired of always having to work hard in a headwind.

I know, obviously, that nobody wants to read about me whinging; there are those who have it much, much, MUCH worse. And you may rest assured I have no intention of doing more of it - I am just being transparent. Something has to give soon. If I were offered a chief strategy officer role or similar again, particularly at a VC or investment firm, the option would appear a lot more attractive than it has in a very long time indeed.

I am not saying, I am just saying.

Anyway.

Before we finally move on to today’s topic, a quick comment on the odd cadence of late. No, there will be no Boyd today either. The reason is that I have been absolutely drowning in requests for AI commentary recently, which is why I felt I needed to write something. The constraints that Substack puts on formatting, including length, meant that there was no space for anything else.

To make up for the lack of exclusive content, the next two newsletters will be premium only. And yes, this means that all analysis pertaining to the work of John Boyd and his OODA loop, including the concluding expert roundtable discussion, will be paywalled.

I know from feedback that his framework has helped many, but while I will always provide content that is available for all, the reality is that I need to prioritize those who support me financially. Consequently, this series will be and remain a premium subscriber exclusive.

Fortunately, if you want to become one, it is easy: just click the link at the bottom of the page.

Moving, at long last, on.

The gen-AI challenge

The predictability of unpredictability and 4E dynamics

Once upon a time - which happened to be roughly twelve months ago - a dashing middle-aged newsletter prince/grumpy old fart of a strategist delivered a keynote presentation at Techsylvania, the largest tech conference in Eastern Europe. Against the backdrop of an AI stampede in which other speakers practically fell over one another to provide the most extravagant prophecies of what would come to be, I explained the inherently unpredictable nature of breakthrough innovation.

My thesis, built upon the works of Brian Arthur and Stuart Kauffman in particular, went as follows: any new technology that comes to exist must be built on an existing technology; innovation is recombination. However, its precise form is inherently impossible to predict. Whenever we are dealing with the complex, indefinite possibilities mean that we cannot know beforehand what events might unfold. The only thing that we can know for certain is that the space of the possible (what can come to be) is significantly larger than the space of the actual (what does come to be).

But, and this is a very important but, it is entirely possible to predict what patterns will emerge once a breakthrough has been made.

One may illustrate this with an addendum to the thought experiment known as Kauffman’s screwdriver. To recap for those who have joined over the years since we first discussed it, if you were to ponder all the possible uses of a screwdriver, you might think of screwing in a screw. Perhaps you would use it to open up a can of paint, as a rudimentary drumstick, to scratch your back, or to prove a point in a newsletter about strategic management. Whatever you come up with, the total number of potential uses, as I alluded to above, is not infinite (you cannot do absolutely anything with a screwdriver) but it is indefinite. Put differently, it is not unlimited but without a specified limit; we do not know what the next use might be before we think of it.

As every new use is also different from the previous, and every context in which the screwdriver is used can be different from the previous, it would be impossible to put the various uses on any kind of scale other than nominal (i.e., one that does not require the use of numeric values or categories ranked by class, but simply unique identifiers). These two premises – (a) the number of uses is indefinite, and (b) each use can only be put on a nominal scale – mean that no algorithm, regardless of its level of sophistication, can calculate all the uses of a screwdriver, nor the next use of a screwdriver. The number is what mathematicians call non-algorithmic. It cannot be pre-stated or predicted a priori. The adjacent possible evolves over time.

Yet if you were to come up with the idea of tying the screwdriver to a pole to make a spear, you would not only be able to fish, but also to create a business: fishing spear rentals. And if you did, instantly, a number of future patterns would become predictable. You would, for example, require a number of keystone services such as sales and accounting. It also stands to reason that others would attempt to replicate your work or come up with improvements.

In other words, even if we cannot predict the invention per se, that which follows in the wake of potential success is, in a sense, predictable. It is not a matter of causality; the unpredictable innovations do not cause predictable patterns to follow. Rather, they enable them. They are not unavoidable causal consequences but adaptive responses to emergent successes, as we know from the law of stretched systems.

The implications are profound, not least for strategy. If we cannot predict what brand, product, or project will take off, but what might happen once one does, we can adjust our behavior accordingly. For example, we are likely going to want to run parallel safe-to-fail experiments and scale fast only once when we have learned what works and why. This has the added benefit of helping us avoid points of potential irreversibility.

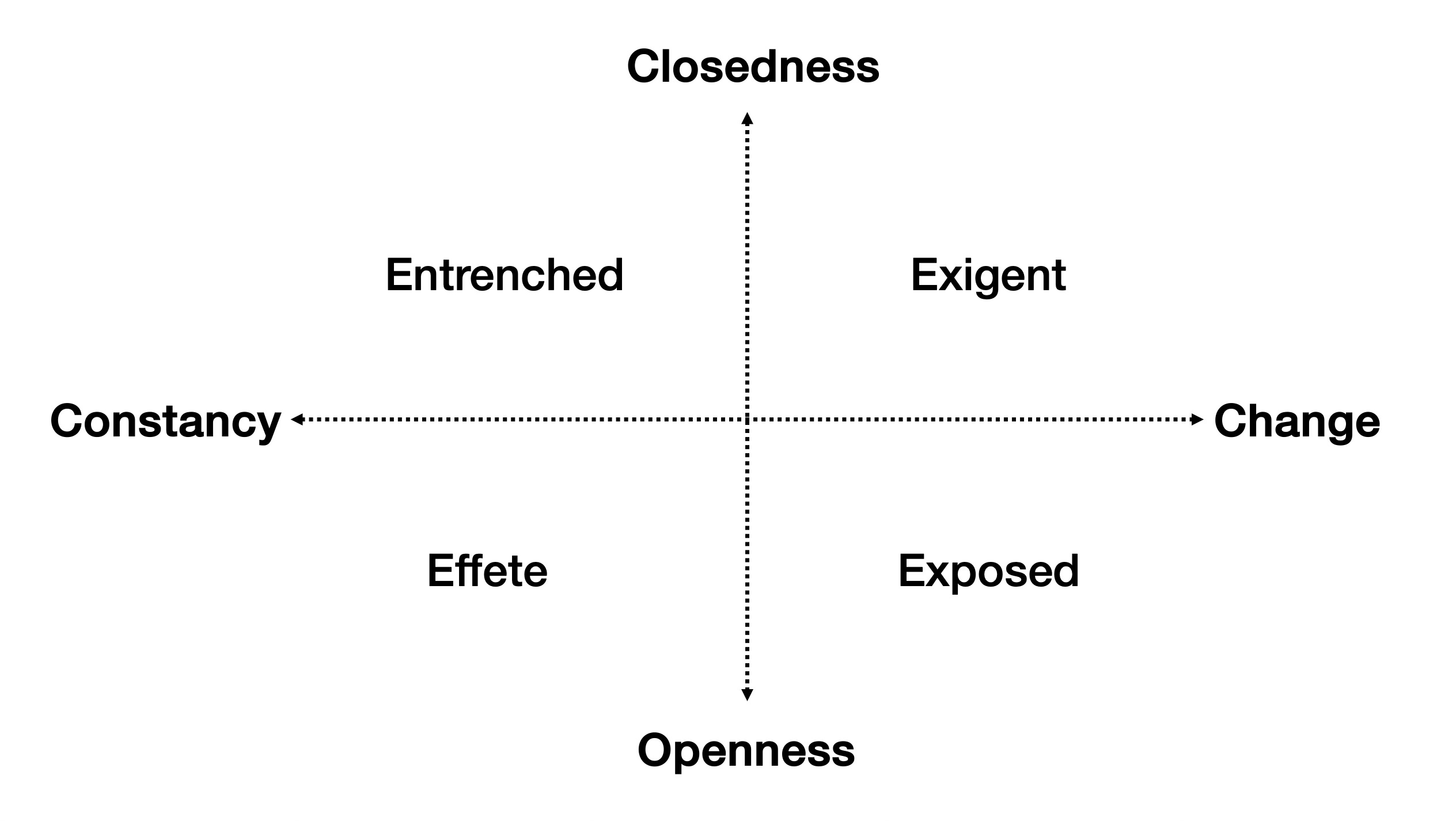

Crucially, though, where the points may be found will inevitably vary from one company to the next, as what may be deemed “safe” to fail does. One may illustrate this through the (very humbly named) Castlin 4E model of market dynamics, as I did in the March 1 premium subscriber newsletter.

As we can see, some markets are exigent, i.e., demarcated by a combination of high change and high barriers to entry. These traits practically ensure that only a select few firms are capable of playing, but also that the potential payoff is significant. No companies are willing to bet large amounts in volatile environments without the allure of returns that justify it.

A case in point is generative AI. The rapidly changing market has proven capable of creating huge upswings in value and growth, yet building a large language model will typically set you back billions of dollars. In fact, as we discovered last week, the leaders in the field have begun to surpass $50B capex figures - which means that artificial intelligence officially has overtaken oil as the most capital intensive industry on the planet. Microsoft and Google now both match Saudi Armaco, the largest player by some distance, in spend. Meta’s lower capex budget will still roughly be that of Exxon Mobil and Chevroned combined. Data really is the new oil after all.

The immense (and escalating) capital expenditures mean that for all the money currently being poured into Silicon Valley gen-AI startups, for some, it still may not be enough. That is not to say that any company would (or should) begin its journey with the budget of Microsoft or Google, but the fact that so few have been able to translate their work into solutions that anyone would actually want to buy is nonetheless telling. As Berber Jin recently highlighted in The Wall Street Journal, a long row of companies (e.g., Imbue, Inflection AI, Cognition, and Character AI) have received hundreds of millions of dollars in investment, with little or no revenue to show for it.

Put differently, the adjacent possible is currently constrained in such a way that small-to-large scale disruption becomes less likely. Unlike what one might call traditional software development, which always was relatively inexpensive (belonging to the exposed category in the aforementioned 4E model), gen-AI bot training consumes colossal amounts of resources. As the CEO of chip-manufacturer Arm, Rene Haas, explained earlier this year, the more information the bots gather, the smarter they become, but the more power they require. If the power grids are unable to keep up with the demand, many small companies will struggle to keep up with the bills. Then, there is the talent issue. The best data scientists (among the few who exist) are hired by the large companies and instantly paid astronomical salaries. The rest are left with, well, the rest.

This presents an obvious challenge. Costs typically come down as technologies mature - another predictable pattern - but we are neither there yet nor even moving towards it. If anything, the current phase represents the opposite. Not only are there financial demands but their size and scope are increasing (at least for initial development). To many, therefore, the situation is analogous to climbing a mountain that keeps growing; even with better equipment, there is no guarantee of relative progress. For all the cash being spent, a hell of a lot of it will go to ventures that have no realistic future trajectory except into absolutely nowhere. As the path to the unpredictable breakthrough becomes ever more expensive, the experiments required are no longer safe to fail for anyone but the already dominant.

Perhaps I should emphasize that the most likely pattern is still that we will see a change over time. Eventually, the costs will come down. The technology will become democratized, at which point the failure rate that markets can afford, but individual companies regardless of size cannot, will ensure that exaptive recombinations and breakthrough innovations eventually emerge. Amara’s law will once again prove correct. We will have over-estimated the impact of the technology in the short-term (not least because so many, as usual, believed those who had financial incentives to promote a hyperbolic narrative), but under-estimated the impact of the technology in the long-term (primarily due to, at the time, yet unrealized adjacent possibles). Plus ça change.

But for now, the situation is what it is.

Hence, for those acquiring the technology in the form of various services, it is important to recognize that the providers of today may not be the providers of tomorrow in nearly literal terms. Building an entire business function, or more, on the promises of a yet-to-be profitable startup is and will, at least in the near-term, continue to be fraught with danger.

The same applies in principle to those investing in it. The smart will adapt while the rest complain about an unsustainable funding climate - an understandable (and even entirely justifiable) claim that ignores that it always is for some but not for others; shifting contextual constraints determine what group specific firms belong to at any given moment.

At the end of the proverbial day, there are and forever will be numerous kinds of constraints that strategists, regardless of where they sit, have to factor in. The 4E model can provide a basic understanding of some of them, and enable us to speculate on things such as the continued volatility of stock prices as the market becomes a prisoner of its own actions. But the only thing that we can know for certain is that artificial intelligence remains in its infancy. We can thus safely predict that there will be both leaps in development and growing pains ahead - even though, as Kauffman’s screwdriver demonstrates, we will never be able to predict their precise nature.

You can either prepare for that reality or attempt to ignore it. I suspect that you are able to surmise which one I would recommend.

Until next time, have the loveliest of weekends.

Onwards and ever upwards,

JP