Friends,

I hope that all is well with you and yours, and that this e-mail finds you on a boat with shoddy connection, in the tropics, three months after I sent it.

Now accepting keynotes for 24Q1-24Q3

Every year, I create three main presentations. For 2024, they are:

What to Do When You Don’t Know What to Do: How to thrive in an uncertain world.

Regression Toward the Meme: Why modern leadership falls into old traps - and what to do about it.

The Efficiency Illusion: Uncovering the hidden costs of digital commerce.

If you want to book me for your event, workshop, or corporate speaking slot, just send me an email. To make sure I am available, however, please do so at your earliest convenience; my schedule is filling up fast - and I will be raising my prices on January 1.

All presentations are adapted to fit the event. Entirely customized presentations, including topic, are available upon request at an additional cost. More information can be found here.

A couple of updates before we go-go

In a turn of events that Mr Magoo would have seen coming a mile away, my wife and I both came down with colds. At the time of writing - and in what I am aware could very well be famous last words - I appear to have dodged the worst of it. The Mrs., on the other hand, have had to spend a couple of days completely knocked out.

Well, I write completely knocked out. Mothers really have superhuman powers. Even though she was feeling unwell, she still mustered enough energy to entertain the young one with things like finger painting, puzzle together-putting, and gingerbread house building.

On a related note, it is common for parents to rave about how much they enjoy experiencing iconic events from their own lives (e.g., watching the original Star Wars or going to their first football game) once more through their children. Obviously, it is just as much about them as it is about their offspring, but it begs the question why adults so seldomly grant themselves permission to be kids, so to speak.

I would imagine that there are many reasons why people stop doing things like building their own gingerbread houses for Christmas, but far from all make sense, particularly if it is a harmless creative endeavor that they enjoy. Allowing the inner kid to come out and play every now and again would do a lot of people good, I suspect.

Moving on.

Where do you draw the line?

How to deal with the patterns of an unpredictable future

Last week, we once more repeated a point already made numerous times before: adaptive strategy, such as ABCDE, centers on movement. The argument is simple. Given that all firms exist on a time continuum between inception and demise, and that cessation of movement is equal to the latter, dynamism is per definition paramount for both survival and prosperity.

Crucially, though, adaptive strategic movement is not about running fast all the time, but enabling the capacity to run fast when needed. Sometimes, that will require the company to first slow down. Attempting to do too much can easily turn into butter scraped over too much bread. Resources are finite. We cannot do everything, nor cover every base; it is financially impossible.

The key question is therefore one of line-drawing. How much is too much? How can we know what to focus on and what to ignore; what to prepare for and what to leave aside? What factor is going to prove pivotal to the long-term success to our efforts, or provide the blow from which we cannot come back?

The answer is that we unfortunately cannot know for certain in advance.

The reason, of course, is that we are dealing with complexity and thus have to consider the principle of the adjacent possible. It is a concept we have covered at length before, but to refresh our minds, it can be defined as what can come to be in any given context; that which is one step away from what currently is.

The space of the possible (what can come to be) is dramatically larger than the space of the actual (what does). One may illustrate this, as Stuart Kauffman has, through basic protein acids - only a fraction of all possible combinations have come into existence, and how nowhere near all will. There are simply too many possible variations:

Recall that if we ask how many proteins, which are linear chains of amino acids, there are with 200 amino acids in the chain, and 20 kinds of amino acids, the answer is 20 raised to the 200th power, or about 10 raised to the 260th power. In a previous post I noted that if the 10 to the 80th particles in the known universe were to do nothing on the shortest, Planck, time scale of 10 to the -43 seconds but make proteins length 200, it would take an astonishing 10 to the 39th power times the 13.7 billion year history of the universe to make all these possible proteins just once.

That is to say, even if the universe did nothing but produce a protein variation of one particular kind (200 amino acids in a chain; 20 different possible acids) once every 10-43 seconds - the shortest time scale known to science - it would require its entire existence, from the Big Bang to the present, to make each variation once. Once!

And if that is not enough to blow your mind, consider this: in Kauffman’s example, the sample space (how many variations of a particular length of protein chain there can be) is known. In complex adaptive systems such as markets, it is not. While the events that can unfold are not infinite, they are indefinite; they are not limitless, but without a definable limit. From this follows that it is impossible to calculate the probability of market occurrences with perfect accuracy regardless of the amount of data collected; the number of potential events is non-algorithmic. The future remains something we cannot entirely plan for a priori.

So.

Do these scientific facts mean that strategy is no more than a lottery, and that the best we can hope for is to be lucky? Well, not exactly. While luck certainly plays a part in any company’s fortunes, there are things that we can do to improve our odds.

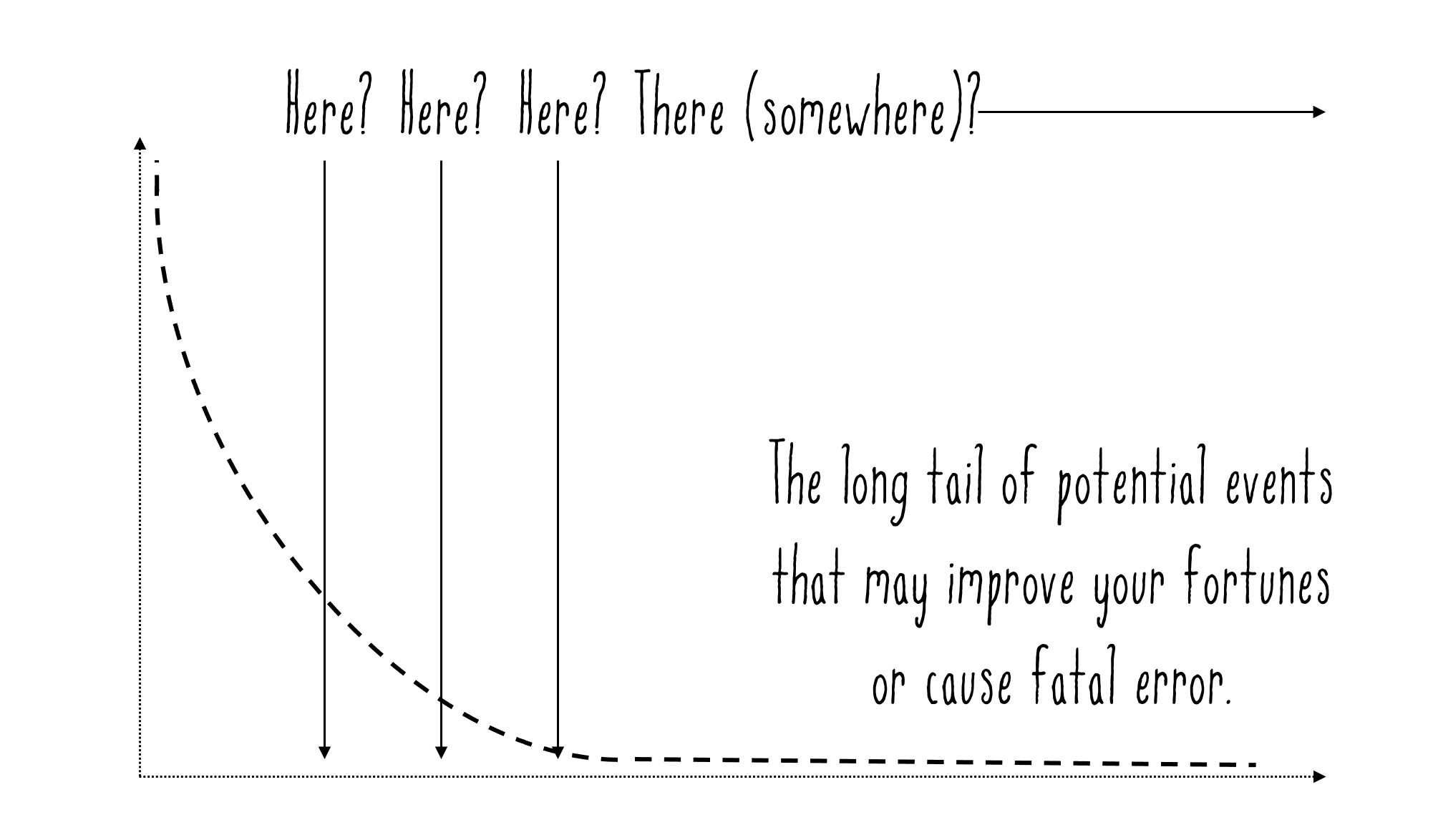

First, we can attempt to identify emergent patterns. Complex systems are not causal, but they are dispositional, i.e., they are pre-disposed to behave in a distinct way. More often than not, as proven by Benoit Mandelbrot, these patterns tend not to be Gaussian (shaped like a bell) but Paretian (shaped like a banana):

The events with the highest frequency sit on the left side of the graph: the 20% that provide 80% of the impact per Pareto rule fame. These are relatively easy to spot. But then there is a long tail of events that are also possible within the adjacent possible, most of which we are unable to foresee.

This is not groundbreaking information by anyone’s stretch of the imagination; most companies of decent stature already know all of it. But many also draw the wrong conclusions about what to do as a result.

Historically, firms (whether via their strategy or risk management department) have dealt with the issue through robustness; they focus on a few key aspects that they perceive themselves able to control, and imagine that as long as they do them well enough, the rest will become irrelevant. Alas, this merely leads to the aforementioned crucial conundrum: how do we know where to draw the line between that which we address and that which we ignore? How well is well enough?

A superior approach is to recognize that certain parts may be more or less stable but that other parts may never be. For companies, this means that while there will be aspects of the business that we know rather well (our present core), it will nonetheless remain important to run coherent safe-to-fail experiments at the edges. In so doing, we may not only discover previously unknown opportunities and risks, but also create necessary resilience over time.

Second, we can safely assume that there will always be surprises; no list of things that can go right or wrong will ever be complete. To illustrate, before Elon Musk’s SpaceX shuttle suffered a “rapid unscheduled disassembly”, his team of rocket scientists had defined the ten largest risks associated with the launch. They ensured that the top five were addressed. The sixth proved to cause the explosion. Similarly, before the Fukushima nuclear disaster, a group of senior engineers had run a pre-mortem exercise (of the kind that we have discussed previously) in which they had listed the twelve most likely causes of a nuclear catastrophe. They prepared for eleven of them. The rest is history.

The point holds as long as complexity is a factor. Nothing, whether strategically or operationally, will ever be wholly fail-safe (as Musk learned when his second rocket blew up as well, even though the team by then had sorted out “number six”). There will always be things that fall outside of the list; there will always be blind spots; there will always be holes in the proverbial bucket. Not all will be potentially catastrophic in nature, naturally (we clearly can build rockets that make it into space), but some may be.

And so, we have to learn how to become adaptive whenever we are dealing with matters that are outside of our control, while admitting that those matters are and forever will be far greater in number than we would ideally like them to be.

Change is not a contrast but a constant. How we deal with it has a decisive impact on the outlook of our organizations. We cannot rely on one thing, but nor can we do everything - and that is why strategy is such a fascinating field to work in.

Next time, we will take our annual look back at the year that has been. Until then, have the loveliest of holidays.

Onwards and upwards,

JP

This newsletter continues below with additional market analyses exclusive to premium subscribers. To unlock them, an e-book, and a number of lovely perks, simply click the button below. If you would rather try the free version first, click here instead.